Prepping to Sell Your Company: What Strategic Buyers Look For Before They Sign

Most CEOs preparing for a transaction spend the majority of their time on the financials. Clean up the books. Show consistent EBITDA. Get the revenue line looking right. That work matters. But it's table stakes.

Strategic buyers, the private equity firms, strategic acquirers, and institutional investors doing serious transactions, are looking at something else entirely. They're looking at the revenue system behind the numbers. And in most mid-market B2B companies, that system doesn't hold up to scrutiny.

This is where valuation gets made or lost. Not in the P&L. In everything the P&L can't explain.

The Due Diligence Nobody Prepares For

Financial due diligence is well understood. Most CEOs have advisors who walk them through it. Revenue due diligence is less understood, less often prepared for, and more often the reason a deal prices lower than expected or gets restructured at the last minute.

The right buyers are asking a specific set of questions that go beyond the numbers. Can this business grow without the founder driving every relationship? Is the pipeline real, documented, and repeatable? Does the messaging hold up when someone other than the CEO is in the room? Can we sell this acquisition to our own stakeholders once we own it?

If the answers to those questions are unclear, the buyer discounts the deal. Sometimes significantly. Not because the business is bad. Because the revenue story can't be verified.

What They're Looking At

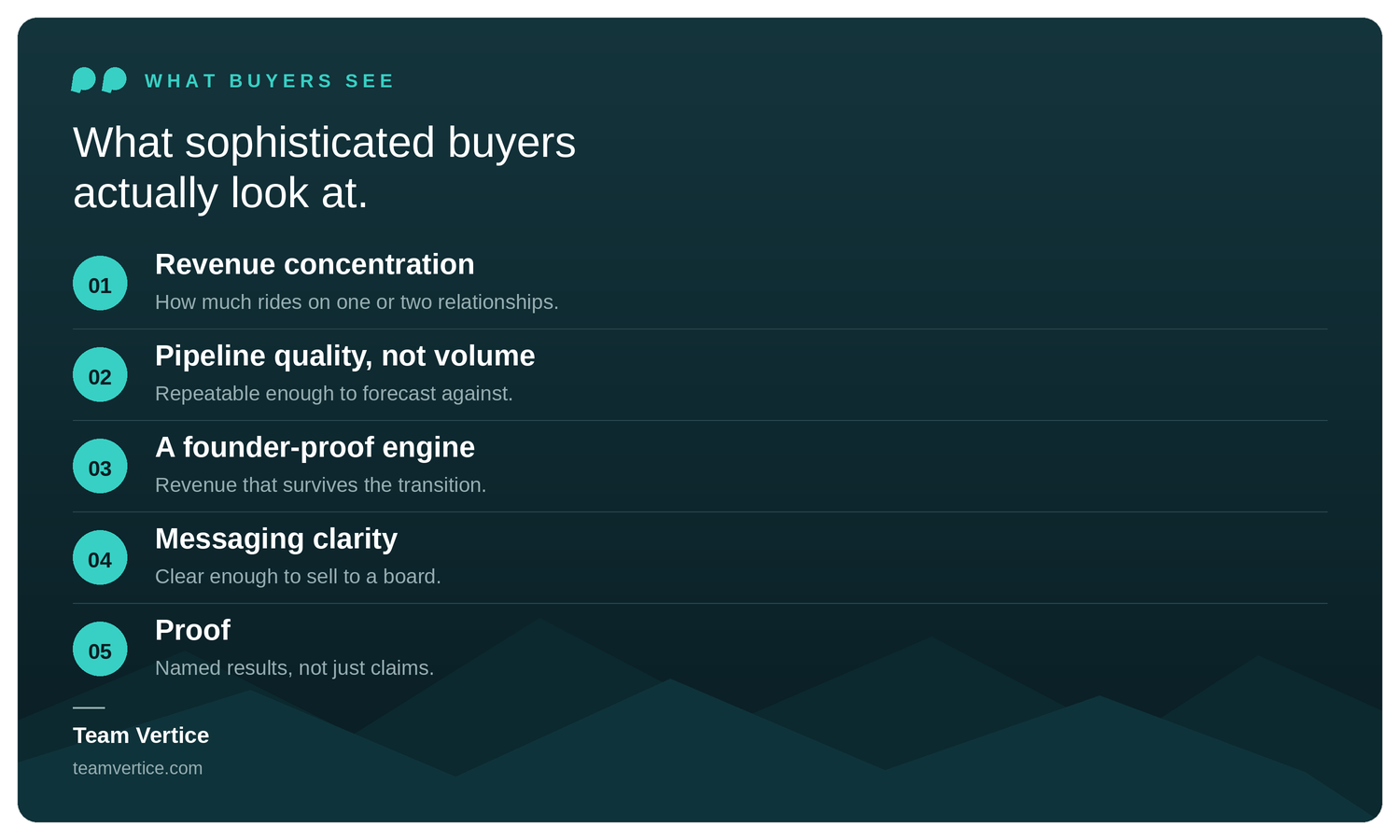

There are five things sophisticated buyers examine that most sellers don't adequately prepare.

The first is revenue concentration. If a meaningful portion of revenue comes from one or two relationships, buyers treat that as risk, not strength. They'll ask how those relationships were built, whether they're contractual or personal, and what happens to them post-close. If the honest answer is that those relationships exist because of the founder's personal network, the buyer will price that dependency into the deal.

The second is pipeline quality and predictability. Not pipeline volume. Quality. A buyer wants to see that the company knows where its next ten deals are coming from, that those opportunities were generated by a system rather than heroics, and that the conversion rates are consistent enough to forecast against. A CRM full of stale opportunities and optimistic close dates is a liability, not an asset.

The third is whether the sales and marketing engine operates independently of the founder. This is the most common failure point in mid-market transactions. The CEO is the best salesperson in the company. The CEO owns the relationships. The CEO closes the big deals. That's not a growth engine. That's a single point of failure. Buyers discount or escrow founder-dependent revenue because they can't count on it surviving the transition.

The fourth is messaging clarity. Buyers have to sell the acquisition internally and externally. They need to be able to explain what the company does, who it serves, and why it wins. If the positioning is murky or the value proposition requires a 45-minute explanation, the buyer starts to wonder if the growth story is real. A company that can't be described in a sentence is harder to integrate, harder to sell to new customers, and harder to pitch to a board.

The fifth is proof. Case studies, documented outcomes, named results. A strong revenue claim means nothing without evidence that the results are repeatable across multiple clients and scenarios. Buyers want to see that the company has a track record, not just a track.

The Multiple You're Leaving on the Table

Every one of these gaps costs money. Not theoretical money. Real multiple compression at the table.

Undocumented pipeline tells a buyer the revenue is lumpy and hard to forecast. That's a lower multiple. Founder-dependent relationships tell a buyer the business doesn't survive the transition cleanly. That's an escrow or an earnout. Weak messaging tells a buyer the growth thesis is harder to execute post-close. That's a lower offer or a longer negotiation.

The CEOs who command premium valuations are the ones who treated exit readiness as a management priority, not a transactional event. They built the systems, documented the process, and cleaned up the revenue story two to three years before anyone started writing term sheets.

The CEOs who don't are the ones who find out what they left on the table after the deal closes.

Exit Readiness Is a Two-Year Build

The single most common mistake in pre-transaction preparation is starting too late. Twelve months out is not enough time to fix structural problems in a revenue system. You can clean up data. You can refresh the pitch deck. You can run a few case studies through the marketing team. But you can't build a repeatable pipeline, establish credible positioning, or separate the founder from the revenue engine in twelve months.

Twenty-four to thirty-six months is the right window. That's enough time to document the pipeline process, validate the ICP against real closed revenue, build content that proves the outcomes, and install the systems a buyer needs to see operating independently.

The work isn't complicated. A documented sales process. A defined ICP. Messaging that holds up in the market. A demand generation system that doesn't depend on one person. Case studies that prove the claims. These aren't difficult things to build. They're just things most companies haven't built yet because nobody pushed them to.

A transaction is the push. The problem is that by the time most CEOs feel that push, they don't have enough runway to do the work properly.

Start Before You Think You Need To

If there's a transaction somewhere on the three to five year horizon, the time to start is now. Not when the banker calls. Not when the board starts asking questions. Now.

Get an honest external assessment of the revenue system. Not just the financials. The messaging, the pipeline, the sales motion, the ICP, the content. Find out what a sophisticated buyer would find if they looked today. Then spend the next two years fixing it.

The companies that do this don't just get better valuations. They build better businesses. The same systems that make a company attractive to a buyer make it easier to run, easier to scale, and easier to lead.

Exit readiness and growth readiness are the same thing. The buyers just make it obvious.

If a transaction is on your 3-5 year horizon and you want to know what a buyer would find in your revenue system today, shoot us a note - we happy to take a look and provide insights.